1

Interim Results of the 2024 Filing Season

April 30, 2024

Report Number: 2024-408-024

This report has cleared the Treasury Inspector General for Tax Administration disclosure review process and information determined

to be restricted from public release has been redacted from this document.

TIGTACommunicat[email protected] | www.tigta.gov

TREASURY INSPECTOR GENERAL FOR TAX ADMINISTRATION

HIGHLIGHTS: Interim Results of the 2024 Filing Season

Final Audit Report issued on April 30, 2024 Report Number 2024-408-024

Why TIGTA Did This Audit

This audit was initiated to provide

selected information related to the

IRS’s 2024 Filing Season. The

overall objective of this review was

to evaluate whether the IRS timely

and accurately processed

individual paper and electronically

filed (e-filed) tax returns during the

2024 Filing Season.

Impact on Tax Administration

The annual tax return filing season

is a critical time for the IRS because

this is when most individuals file

their income tax returns and

contact the IRS if they have

questions about specific tax laws

or filing procedures.

The IRS began processing Tax

Year 2023 individual tax returns

on January 29, 2024. During

Calendar Year 2024, the IRS

expects to receive 167.1 million

individual income tax returns.

The total e-file volume is projected

to increase by 3.7 million

(2.4 percent) in Calendar

Year 2024.

In addition, the IRS’s fraud

detection processes continue to

prevent the issuance of a

significant amount of fraudulent

refunds.

What TIGTA Found

As of March 2, 2024, the IRS received more than 54 million tax

returns, of which 52.8 million (97.7 percent) were e-filed. The IRS also

issued refunds totaling $115.5 billion. In addition, as of this same

date, the IRS received more than 1.1 million Free File returns, which is

a 14 percent increase as of the same period during the 2023 Filing

Season.

TIGTA’s review of the IRS’s business rules determined that 44 of the

56 rules are accurately rejecting tax returns or were intentionally

disabled. Two business rules were incorrectly rejecting tax returns,

and 10 business rules had either low or no rejections. As such, TIGTA

will continue to monitor them throughout the remainder of the filing

season. TIGTA’s review of the accepted e-filed tax returns identified

no concerns that tax returns with the conditions described in the

56 business rules were accepted erroneously for processing.

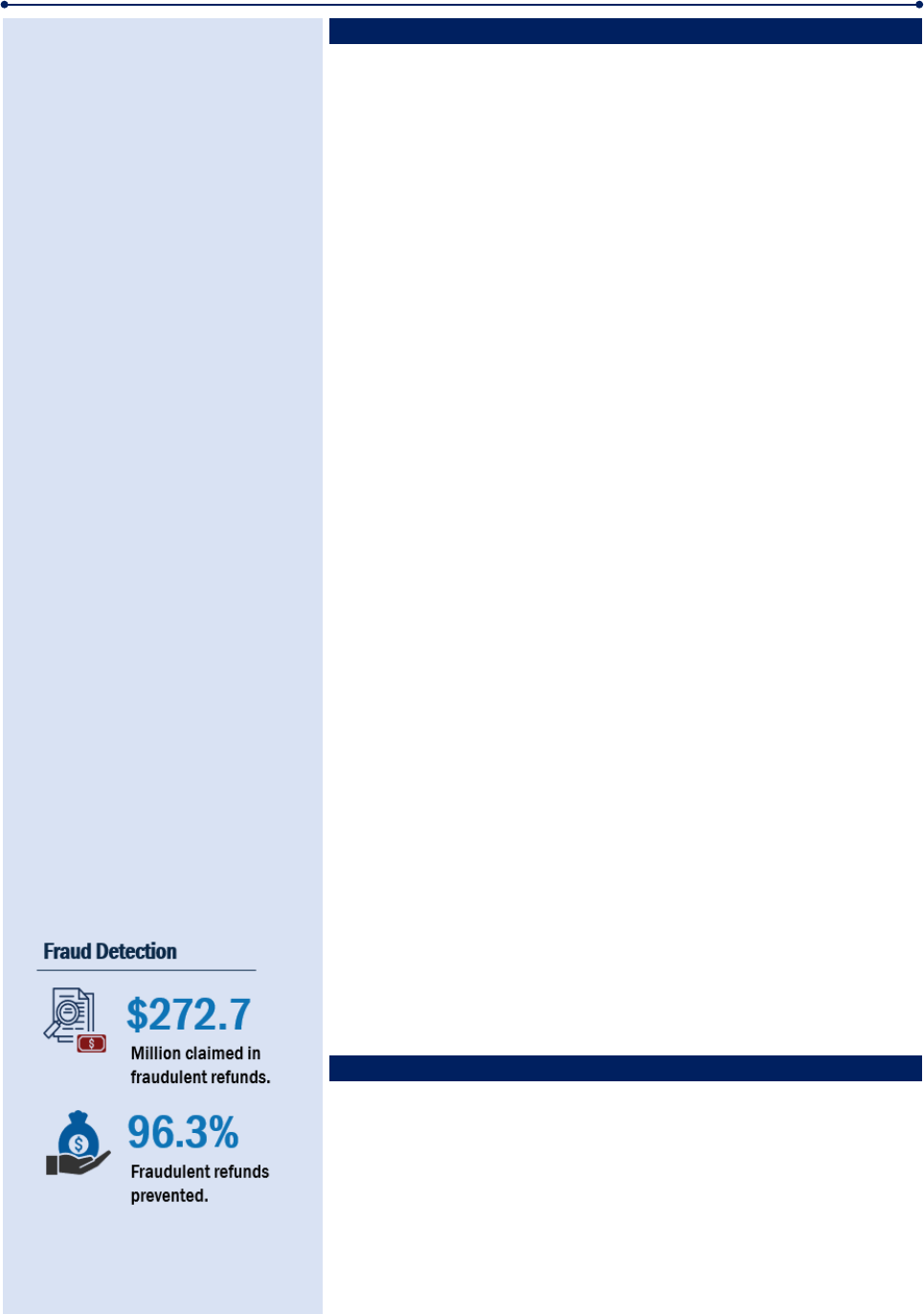

The IRS continues to increase the number of fraudulent tax returns

detected and stopped from entering the tax processing system,

i.e.

,

rejecting e-filed tax returns and preventing paper tax returns

from posting. In addition, as of February 24, 2024, the IRS reported

that it identified 32,616 tax returns with approximately $272.7 million

claimed in fraudulent refunds and prevented the issuance of

$262.7 million (96.3 percent) of those refunds.

In addition, the IRS provides assistance to millions of taxpayers via its

website (IRS.gov), telephone, and social media platforms as well as

face-to-face assistance at its Taxpayer Assistance Centers, Volunteer

Income Tax Assistance sites, and Tax Counseling for the Elderly sites.

Finally, the IRS offers taxpayers the ability to obtain information using

their mobile devices. For example, the IRS uses common social

media platforms to share the latest information on tax changes, scam

alerts, initiatives, and products and services.

As of March 2, 2024, taxpayers made 18.4 million total attempts to

contact the IRS by calling the various customer service toll-free

telephone assistance lines. The IRS reports that 4.1 million calls were

answered with automation, and telephone assistors answered nearly

4.3 million calls and provided a 91 percent Level of Service with a

2-minute Average Speed of Answer. The Level of Access, which

TIGTA previously developed because the IRS’s Level of Service

measure did not reflect overall call demand, was 51.2 percent.

What TIGTA Recommended

This report was prepared to provide interim information only.

Therefore, no recommendations were made in this report.

U.S. DEPARTMENT OF THE TREASURY

WASHINGTON, D.C. 20024

TREASURY INSPECTOR GENERAL

FOR TAX ADMINISTRATION

April 30, 2024

MEMORANDUM FOR: COMMISSIONER OF INTERNAL REVENUE

FROM: Matthew A. Weir

Acting Deputy Inspector General for Audit

SUBJECT: Final Audit Report – Interim Results of the 2024 Filing Season

(Audit No.: 2024408023)

This report presents the results of our review to evaluate whether the Internal Revenue Service

timely and accurately processed individual paper and electronically filed tax returns during the

2024 Filing Season. This review is part of our Fiscal Year 2024 Annual Audit Plan and addresses

the major management and performance challenges of

Tax Law Changes

,

Managing IRA

Transformation Efforts

,

and

Taxpayer Service

.

This report was prepared to provide information only. Therefore, we made no

recommendations in the report. However, we provided Internal Revenue Service management

officials with an advance copy of this report for review and comment prior to issuance.

If you have any questions, please contact me or Diana M. Tengesdal, Assistant Inspector General

for Audit (Returns Processing and Account Services).

Interim Results of the 2024 Filing Season

Table of Contents

Background .....................................................................................................................................Page 1

Results of Review .......................................................................................................................Page 3

Processing Tax Returns

Individual Tax Return Receipts and Number of Refunds

Issued Decreased Slightly From the 2023 Filing Season .......................................Page 3

Detecting and Preventing Tax Refund Fraud

Fraud Detection Processes Continue to Prevent and Detect

the Issuance of Millions of Dollars in Fraudulent Refunds ...................................Page 7

Providing Customer Service

IRS Customer Service Initiatives

.....................................................................................Page 9

Appendices

Appendix I – Detailed Objective, Scope, and Methodology ................................Page 15

Appendix II – Treasury Inspector General for Tax Administration

Audits of Inflation Reduction Act of 2022 Tax Law Changes ..............................Page 17

Appendix III – Electronic Filing Business Rules ........................................................Page 18

Appendix IV – Tax Return Errors Resolved Using the FixERS Tool ...................Page 23

Appendix V – Glossary of Terms ....................................................................................Page 26

Appendix VI – Abbreviations ...........................................................................................Page 29

Page 1

Interim Results of the 2024 Filing Season

Background

The annual tax return filing season is a critical time for the Internal Revenue Service (IRS)

because it is when most individuals file their income tax returns and contact the IRS if they have

questions about specific tax laws or filing procedures.

1

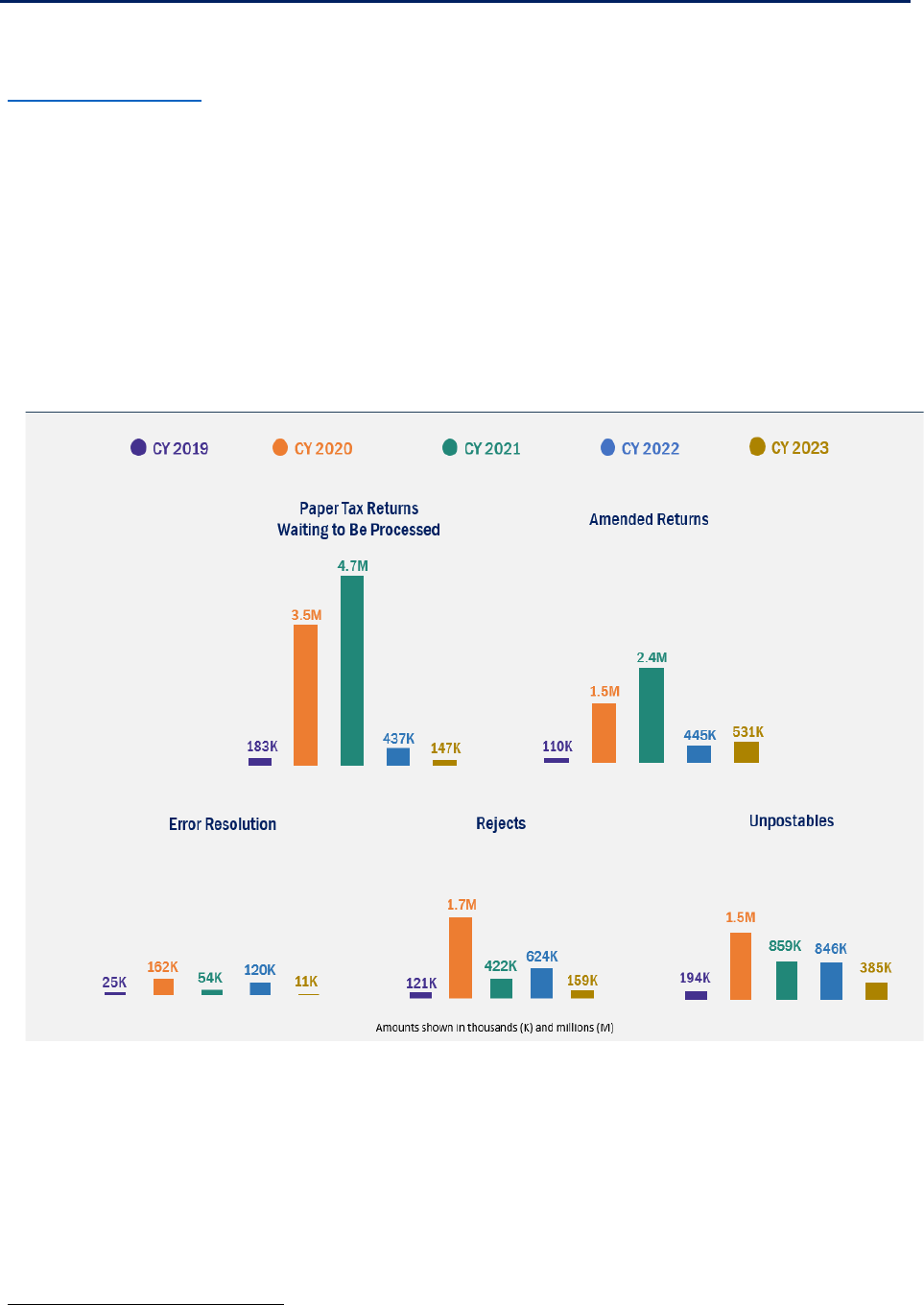

While the IRS has reduced most

inventories at or near pre-Pandemic levels, the unpostable and amended tax return inventories

remain at higher levels. Figure 1 provides a comparison of individual tax return inventory levels

in various stages of processing that the IRS normally carried into the subsequent years’ filing

season compared to inventory levels carried into the 2024 Filing Season.

Figure 1: Comparison of Individual Return

Inventory Carried Over to the Next Filing Season

Source: IRS Filing Season Statistics Report for the week ending December 28, 2019; IRS inventory

numbers provided to the Treasury Inspector General for Tax Administration (TIGTA) for the weeks

ending December 29, 2020, December 28, 2021, December 30, 2022, and December 29, 2023;

and the Customer Account Services Form 1040X Consolidated Inventory Report for the weeks

ending December 28, 2019, December 26, 2020, January 1, 2022, December 31, 2022, and

December 30, 2023. CY = Calendar Year. Amended Returns = Form 1040-X, Amended U.S. Individual

Income Tax Return.

1

See Appendix V for a glossary of terms.

Page 2

Interim Results of the 2024 Filing Season

Key tax law changes affecting the 2024 Filing Season

One of the continuing challenges the IRS faces each year in processing tax returns is the

implementation of new tax law changes as well as changes resulting from expired tax provisions.

The primary legislation affecting the 2024 Filing Season is the

Inflation Reduction Act of 2022

(IRA), signed into law on August 16, 2022.

2

While many IRA provisions have been implemented

since being signed into law, a small number of provisions affect individual tax filers for

Tax Year 2023. Figure 2 identifies the three provisions most relevant to the 2024 Filing Season

and provides the estimated tax impact for each provision for Calendar Years 2024 through 2027.

Figure 2: Summary of IRA Provisions Affecting the 2024 Filing Season

Provision Overview of Related Provisions

Tax Impact

Calendar

Years

2024 – 2027

Energy Efficient Home

Improvement Credit

(13301)

Renamed and replaced the existing Nonbusiness Energy

Property Credit and extended the credit to property placed in

service through December 31, 2032.

$5.3 billion

Residential Clean

Energy Credit (13302)

Renamed and replaced the existing Residential Energy

Efficient Property Credit and increased the credit rate to 30

percent for property placed into service beginning in Tax Year

2022.

$9.3 billion

Alternative Fuel

Refueling Property

Credit (13404)

Modified the existing credit for certain refueling property

placed into service after Calendar Year 2022.

$621 million

Source: The IRA and the Joint Committee on Taxation JCX-18-22.

We have separate audits that will address the IRS’s implementation of Clean Vehicle Credits,

Elective Payments and Credit Transferability, and the Direct File Pilot Program.

3

In addition, we

are monitoring potential legislation such as the

Tax Relief for American Families and Workers

Act, 2024

. If enacted, the legislation would increase the refundable portion of the Child Tax

Credit (CTC) from $1,400 to $1,800 for Tax Year 2023, $1,900 for Tax Year 2024, and up to $2,000

for Tax Year 2025. Annual inflation increases would impact the credit beginning after Tax

Year 2023. During recent testimony, the IRS Commissioner stated that if the legislation is

enacted, it will take six to 12 weeks for the IRS to implement the changes and complete the

adjustments to tax accounts.

4

Additionally, the Commissioner expects only 10 percent of

households will be affected by the adjustment, which will allow the IRS to complete the

adjustments quickly.

TIGTA reports on IRS Strategic Operating Plan and new organizational structure

In March 2024, TIGTA reported that the IRS publicly released its Strategic Operating Plan on

April 6, 2023, noting that the plan outlines how the IRS will deliver transformational change for

2

Pub. L. 117-169, 136 Stat. 1818.

3

See Appendix II for a list of TIGTA audits related to IRA tax law changes.

4

Hearing with Commissioner of the Internal Revenue Service, Daniel Werfel Before the H. Comm. on Ways and

Means

, 118th Cong. (2024).

Page 3

Interim Results of the 2024 Filing Season

taxpayers.

5

The Strategic Operating Plan outlines five transformation objectives, which are

comprised of 42 initiatives. These initiatives outline how the IRS plans to provide best-in-class

customer service and transform how taxpayers interact with the IRS, modernize technology and

analytics, reduce the Tax Gap by focusing on taxpayers with complex filings and high-dollar

noncompliance, and become an employer of choice.

In addition to the standup of the Transformation and Strategy Office, on December 13, 2023, the

IRS Commissioner announced a new leadership structure noting this was a step designed to

reflect the IRS’s new transformation goals. The new structure, which became effective

April 7, 2024, will help the IRS work efficiently as an agency and ensure that progress keeps

moving forward. The IRS’s new organizational structure features a single deputy IRS

Commissioner and four new IRS chief positions.

As was announced in December 2023, these changes create more specialization at the top of

the IRS’s organizational chart. According to the IRS, the new structure will allow for more

specialization on emerging priorities in the transformation work while strengthening the senior

leadership team’s oversight capability and flexibility on pressing tax administration issues. One

of the four chiefs reporting to the Deputy Commissioner is the Chief, Taxpayer Services. This

position will be responsible for many of the major taxpayer service functions currently handled

by the Wage and Investment Division, including the filing season work and taxpayer-facing

operations such as toll-free operations, tax return processing centers, Taxpayer Assistance

Centers (TAC), tax forms, taxpayer correspondence, and publication development.

Results of Review

This report presents the interim results of our review to evaluate whether the IRS is timely and

accurately processing Tax Year 2023 individual paper and electronically filed (e-filed) tax returns.

The results are presented as of several dates between January 29, 2024, and March 30, 2024,

depending on when the information was available.

Individual Tax Return Receipts and Number of Refunds Issued Decreased

Slightly From the 2023 Filing Season

The IRS began processing individual tax returns on January 29, 2024. During

Calendar Year 2024, the IRS expects to receive up to 167.1 million (nearly 9.5 million paper and

157.6 million e-filed) individual income tax returns. The total e-file volume is projected to

5

TIGTA, Report No. 2024-IE-R010,

Inflation Reduction Act: Continued Assessment of Transformation Efforts –

Evaluation of Fiscal Year 2023 Delivery of Initiatives

(Mar. 2024). This review is part of TIGTA’s continued assessment

of the IRS’s transformation efforts.

Page 4

Interim Results of the 2024 Filing Season

increase by 3.7 million (2.4 percent) in Calendar Year 2024. Figure 3 presents comparative

statistics as of March 2, 2024. The statistics shown for the 2023 Filing Season represent a start

date of January 23, 2023.

Figure 3: Comparative Filing Season Statistics

Cumulative Filing Season Data

2023 Actual 2024 Actual

%

Change

Individual Income Tax Returns

Total Returns Received (000s) 54,948 54,030 -1.7%

Paper Returns Received

(000s)

1,350 1,235 -8.5%

E-Filed Returns Accepted

(000s)

53,598 52,795 -1.5%

Practitioner-Prepared (000s)

25,210

24,516

-2.8%

Home Computer (000s)

28,387 28,279 -0.4%

Free File (000s)

(in the Home Computer total)

1,006 1,147 14.0%

Percentage of Returns E-Filed 97.5% 97.7% 0.2%

Refunds

Total Number Refunds Issued

(000s)

42,040 36,288 -13.7%

Total Dollars

$127.3 billion $115.5 billion -9.3%

Average Refund Amount

$3,028 $3,182 5.1%

Total Number of Direct Deposits

(000s)

39,907 35,369 -11.4%

Total Direct Deposit Dollars

$124.3 billion $114.7 billion -7.7%

Source: Filing Season Weekly Report for 2023 Filing Season figures are through March 3, 2023, and

2024 Filing Season figures are through March 2, 2024. Totals and percentages shown are rounded.

While e-file volumes decreased by 1.5 percent, the number of returns filed through the IRS Free

File Program increased by 14 percent when compared to the same period during the 2023 Filing

Season. We also observed the total number of refunds issued and total dollars decreased by

13.7 percent and 9.3 percent, respectively, when compared to the same period during the

2023 Filing Season. This slight decrease can be attributed to the filing season starting one week

later in Calendar Year 2024 than it did in Calendar Year 2023. In addition, taxpayers may have

delayed filing due to anticipated legislative changes. As of March 30, 2024, e-file volumes have

surpassed the levels they were at as of March 31, 2023. We are currently conducting separate

reviews of both the IRS’s Direct File Pilot and Free File Programs. We plan to issue an interim

report for the Direct File Pilot Program in May 2024 and a final report later in Calendar

Year 2024. The final report will continue to evaluate the volume and accuracy of tax returns

submitted through the Direct File tool as well as the costs to implement the Direct File tool

during the 2024 Filing Season. We will report on the IRS’s Free File Program later in

Calendar Year 2024.

6

Individual tax return inventories

The IRS establishes timeliness goals for its various tax return processing programs that reflect

6

TIGTA, Audit No. 2024408011,

Direct File Pilot Program

and TIGTA, Audit No. 202340028,

Free File Program –

Follow-Up

.

Page 5

Interim Results of the 2024 Filing Season

the desired number of days it should take to work a tax return from receipt in the program’s

inventory. Figure 4 provides the inventory levels in key tax return processing programs as of

March 2, 2024, along with the percentage of the inventory that is aged and the program’s

timeliness goal. The figures provided for paper tax returns and Error Resolution inventories

show work received during Calendar Year 2024 and do not include any carryover work from

previous filing seasons. The figures provided for Rejects, Unpostables, and Amended Returns

represent work that could have been received during calendar years prior to 2024,

i.e.

, Tax

Years 2020 through 2022 returns that have not completed processing, as well as Tax Year 2023

and prior work received during Calendar Year 2024.

Figure 4: Age of Tax Return Processing Inventories

Type of Work Remaining

Week Ending

March 2, 2024

Percentage

Aged

Aged Criteria

Paper Tax Returns 284,586 None N/A

Error Resolution 151,517 0.4 percent Over 5 days

Rejects 496,141 3.4 percent Over 60 days

Unpostables 432,672 43.8 percent

Ranges from more

than 3 weeks to

more than 15 weeks

Amended Returns Worked

by the Submission

Processing Function

455,463 73.1 percent More than 30 days

Amended Returns

Worked

by the Accounts

Management Function

502,368 63.1 percent More than 44 days

Source: IRS-provided weekly inventory levels for the week ending March 1, 2024,

Submission Processing 1040X Inventory Report for the week ending March 1, 2024,

Accounts Management Inventory Report for the week ending March 2, 2024, and Customer

Account Services Form 1040X Consolidated Inventory Report for the week ending

March 2, 2024.

In March 2024, we reported that concerns remain with the inventories of amended tax returns

remaining to be worked, which are significantly above the pre-Pandemic levels.

7

The Accounts

Management function does not set goals specifically for amended individual tax returns

inventories. In our discussions with IRS management, they indicated that the inventories of

amended individual returns remained high because of high attrition and staffing shortages. As

of April 2024, the IRS Submission Processing function estimates that amended individual tax

return inventories will not be back to pre-Pandemic levels until December 2024.

The Accounts Management function surpassed its original hiring goal of 6,431 employees and

increased its target to 6,831. As of March 2, 2024, the Accounts Management function has hired

6,820 employees or 106 percent of its original goal of 6,431. This increase in staff should help

the IRS to decrease the amended tax return inventories discussed previously.

7

TIGTA, Report No. 2024-406-020,

The IRS Continues to Reduce Backlog Inventories in the Tax Processing Centers

(Mar. 2024).

Page 6

Interim Results of the 2024 Filing Season

In contrast, the IRS Submission Processing function is not meeting its hiring goal, but it is

making progress towards that goal. As of March 5, 2024, the Submission Processing function

has onboarded 62 percent of its goal of 3,600 employees. The IRS Submission Processing

function has needed to alter its hiring strategies and take other actions to help balance work

across the Tax Processing Centers. For example, during the 2024 Filing Season, the IRS is

redirecting taxpayers in certain States to mail their tax return to the Austin Tax Processing

Center instead of the Kansas City Tax Processing Center. In addition, the IRS continues to use

Direct Hiring Authority to assist with meeting its hiring goals. We are conducting a separate

review of the IRS’s hiring efforts and expect to issue the report in Calendar Year 2024.

8

Evaluation of new and modified e-file business rules

The IRS uses e-file business rules to identify errors on tax returns at the time the returns are

filed. We selected 56 e-file business rules for in-depth testing that are new or were modified for

the 2024 Filing Season. Our testing evaluated whether the IRS was accurately rejecting tax

returns when applicable, and conversely whether any tax returns were erroneously accepted for

processing. For example, we selected 29 business rules created to address legislative changes

affecting the Residential Clean Energy Credit, Energy Efficient Home Improvement Credit, and

Alternative Fuel Refueling Property Credit. Appendix III of this report contains a list of the

business rules we reviewed.

As of February 9, 2024, our testing of 44 of the 56 business rules found that the majority of the

rules are accurately rejecting tax returns or were intentionally disabled. We also identified two

business rules that were not correctly rejecting tax returns and alerted the IRS of these issues on

February 7, 2024, and March 18, 2024. IRS management agreed the rules were not working as

intended and indicated they would take the necessary corrective actions to fix the programming.

In addition, 10 of the 56 business rules have either had minimal or no rejections of tax returns as

of February 9, 2024. We will continue to monitor and test rules with low or no reject counts,

re-activated rules, or newly implemented rules and will report on their accuracy later in Calendar

Year 2024.

Our review of accepted e-file tax returns identified no concerns that tax returns with the

conditions described in the 56 rules were erroneously accepted for processing. In addition, we

determined the 156 business rules that were documented as being deleted or disabled were

accurately deleted or disabled for Tax Year 2023.

Expansion of the automated Error Resolution correction tool

The IRS implemented an automated Error Resolution correction tool during the 2022 Filing

Season to shorten the time needed to resolve certain taxpayer errors that could delay their

refund as well as to reduce the risk of IRS employee error. The IRS refers to this tool as the

FixERS tool. This tool systemically replaces the steps an IRS Error Resolution employee would

take to resolve the identified tax return errors. The IRS began using the FixERS tool to address

common taxpayer errors when claiming the CTC, the Earned Income Tax Credit, the Child and

Dependent Care Credit (CDCC), and the Recovery Rebate Credit (RRC). IRS management stated

that they chose these errors because they expected tax returns with these errors to be the most

impactful on taxpayers during the 2022 Filing Season.

8

TIGTA, Audit No. 202310812,

Improving the Hiring Process.

Page 7

Interim Results of the 2024 Filing Season

The IRS expanded the FixERS tool to 21 error codes for the 2023 Filing Season and added two

more codes for the 2024 Filing Season, bringing the total to 23 error codes. As of

February 29, 2024, the IRS reports that 493,072 tax returns have been placed into production for

the FixERS tool. From this population, 321,357 (65 percent) tax return errors were systemically

resolved while 171,715 (35 percent) tax return errors were resuspended for manual processing.

Appendix IV of this report contains a complete list and description for the 23 error codes.

Fraud Detection Processes Continue to Prevent and Detect the Issuance of

Millions of Dollars in Fraudulent Refunds

The IRS continues to increase the number of fraudulent tax returns detected and stopped from

entering the tax processing system,

i.e.

, rejecting e-filed tax returns and preventing paper tax

returns from posting. For example, as of December 28, 2023, the IRS has locked taxpayer

accounts of 53.7 million deceased individuals. This compares to 52.5 million accounts locked as

of January 20, 2023. When tax accounts are locked, e-filed tax returns are rejected, and paper

tax returns are prevented from posting to the Master File. According to the IRS, as of

February 29, 2024, it had rejected 31,173 fraudulent e-filed tax returns and had stopped

173 paper tax returns from posting to the Master File as a result of the deceased taxpayer

account locks.

In addition, as of February 24, 2024, the IRS reported that it identified 32,616 tax returns with

approximately $272.7 million claimed in fraudulent refunds and prevented the issuance of

$262.7 million (96.3 percent) of those refunds. This represents a decrease in the amount of

fraudulent refunds stopped when compared to the same period during the 2023 Filing Season,

although the number of refunds identified and stopped increased from the prior year. Figure 5

shows the number of fraudulent tax returns the IRS identified for Processing Years 2022, 2023,

and 2024 as well as the refund amounts that were stopped.

Figure 5: Fraudulent Tax Returns and Refunds Identified

and Stopped in Processing Years 2022, 2023, and 2024

Processing

Year

Number of

Fraudulent

Refund

Returns

Identified

Number of

Fraudulent

Refund Returns

Stopped

Amount of Fraudulent

Refunds Identified

Amount of Fraudulent

Refunds Stopped

2022 76,814 74,711 $817,400,771 $807,903,066

2023 31,079 30,730 $310,724,203 $303,718,702

2024 32,616 30,867 $272,738,111 $262,682,364

Source: IRS fraudulent tax return statistics for Processing Years 2022 (as of February 26, 2022), 2023 (as of

February 25, 2023), and 2024 (as of February 24, 2024).

Page 8

Interim Results of the 2024 Filing Season

Detection of tax returns involving identity theft

For the 2024 Filing Season, the IRS is using 282 filters to detect potential identity theft tax

returns and prevent the issuance of fraudulent refunds. In comparison, the IRS used 260 filters

for the 2023 Filing Season. These filters incorporate criteria based on characteristics of

confirmed identity theft tax returns, including amounts claimed for income and withholding,

filing requirements, prisoner status, taxpayer age, and filing history. Tax returns identified by

these filters are held during processing until the IRS can verify the taxpayer’s identity. If the

individual’s identity cannot be confirmed, the IRS removes the tax return from processing to

prevent the issuance of a fraudulent refund.

As of February 29, 2024, the IRS reported that it identified nearly 1.9 million tax returns with

refunds totaling approximately $16.5 billion for additional review as a result of the identity theft

filters. As of that same date, the IRS had confirmed 15,242 tax returns as fraudulent and

prevented the issuance of $180.5 million in fraudulent refunds. Figure 6 shows the number of

identity theft tax returns the IRS identified and confirmed as fraudulent in Processing Years 2023

and 2024 as of February 29, 2024.

Figure 6: Identity Theft Tax Returns Confirmed

Fraudulent in Processing Years 2023 and 2024

Processing Year Confirmed Identity Theft Returns

2023 12,617

2024 15,242

Source: IRS fraudulent tax return statistics for Processing

Year 2023 (as of March 2, 2023) and Processing Year 2024 (as of

February 29, 2024).

Identity theft protection

The IRS automatically issues an Identity Protection Personal Identification Number (IP PIN) to

confirmed identity theft victims if the case is resolved prior to the start of the next filing season.

Taxpayers nationwide can also request an IP PIN directly from the IRS if they are concerned that

their personal information has been stolen and want to protect their identity when filing a

Federal tax return. The IP PIN is a six-digit number assigned to eligible taxpayers to help

prevent someone else from filing a fraudulent Federal income tax return using a taxpayer’s

Social Security Number (SSN).

9

The IP PIN is known only to the taxpayer and the IRS and acts as

an authentication number to validate the correct owner of the SSN or Individual Taxpayer

Identification Number (ITIN) listed on that tax return. This helps the IRS verify the taxpayer’s

identity when they file their tax return. Taxpayers can request an IP PIN or retrieve their existing

IP PIN by using the “Get an IP PIN” tool through IRS.gov. The IRS reports that it issued

1.1 million IP PINs to taxpayers who used this tool as of February 29, 2024.

9

Anyone who has an SSN or an ITIN and is able to verify their identity is eligible to enroll in the IP PIN program.

Page 9

Interim Results of the 2024 Filing Season

Screening of prisoner tax returns

To combat refund fraud associated with tax returns filed using prisoner SSNs, the IRS compiles a

list of prisoners (the Prisoner File) received from the Federal Bureau of Prisons and State

Departments of Corrections as well as Prisoner Update Processing System data from the Social

Security Administration. These data files are used to identify for additional screening tax returns

filed using a prisoner SSN. As of February 24, 2024, the IRS reported that it identified for

screening 15,189 potentially fraudulent tax returns filed by prisoners.

10

This represents an

increase of 1.7 percent over the number of tax returns identified during the same period of the

2023 Filing Season. Figure 7 shows the number of prisoner tax returns identified for screening

in Processing Years 2023 and 2024.

Figure 7: Prisoner Tax Returns Identified for

Screening in Processing Years 2023 and 2024

Processing Year

Number of Prisoner Tax Returns

Identified for Screening

2023

14,939

2024

15,189

Source: IRS fraudulent tax return prisoner strategy statistics

for Processing Year 2023 (as of February 25, 2023) and

Processing Year 2024 (as of February 24, 2024).

IRS Customer Service Initiatives

The IRS provides assistance to millions of taxpayers via its website (IRS.gov), telephone, and

social media platforms as well as face-to-face assistance at its TACs, Volunteer Income Tax

Assistance sites, and Tax Counseling for the Elderly sites.

Online assistance

The IRS provides easy-to-use self-assistance options that enable taxpayers to access the

information they need 24 hours a day, seven days a week. The most notable self-assistance

option is the IRS’s public Internet site, IRS.gov. The IRS reported 337.3 million visits to IRS.gov

for the 2024 Filing Season as of March 2, 2024. In comparison, the IRS reported 289.8 million

visits to IRS.gov for the 2023 Filing Season as of March 3, 2023, which is an increase of

16.4 percent. The IRS website provides a number of online tools to assist taxpayers. Figure 8

10

Tax returns filed using a prisoner’s name and Taxpayer Identification Number.

Page 10

Interim Results of the 2024 Filing Season

provides examples of these online tools along with the number of times the tool was used as of

February 24, 2024.

Figure 8: Examples of Online Tool Uses for Processing Years 2023 and 2024

(as of Week Ending February 24, 2024)

Tool Description

Number of Uses

in Processing

Year 2023

Number of Uses

in Processing

Year 2024

Interactive Tax

Assistant

A tax law resource that takes taxpayers through

a series of questions and provides them with

responses to basic tax law questions.

0.5 million 0.7 million

Where’s My

Refund?

Allows taxpayers to check the status of their

refunds using the most up-to-date information

available to the IRS.

140.7 million 163.9 million

Where’s My

Amended Return?

Allows taxpayers to check the status of their

amended return using the most up-to-date

information available to the IRS.

1.4 million 1.3 million

Source: IRS management information reports.

The

Where’s My Refund?

and the

Where’s My Amended Return?

tools are available on IRS.gov.

The

Where’s My Refund?

tool is also available on the IRS2Go mobile application. IRS2Go is a

mobile application that allows taxpayers to check the status of their tax refund, make a payment,

find free tax preparation assistance, sign up for helpful tax tips, and access IRS social media

platforms. As of February 29, 2024, the IRS reported nearly 5.2 million active users for the

IRS2Go application. In November 2023, we reported on the planned enhancements the IRS had

for its online tools as part of the Strategic Operating Plan objectives to dramatically improve

services to taxpayers.

11

On February 5, 2024, the IRS confirmed enhancements to the

Where’s

My Refund?

tool were implemented as of January 3, 2024. These enhancements include

modernizing the

Where’s My Refund?

tool to create a consistent experience for taxpayers when

they access other IRS applications, such as online accounts, or when they call the toll-free

telephone line. The enhancements also include tailored messages with information about

common fraud and error conditions, detailed refund statuses in plain language, and notifications

indicating whether the IRS needs additional information. We plan to review these

enhancements and will include the results in our final filing season report later in Calendar

Year 2024.

The IRS also launched a public-facing dashboard on its website, called the

Processing Status for

Tax Forms

, which lists the current processing statuses for general correspondence and key tax

forms

e.g.

, Form 1040,

U.S. Individual Income Tax Return

, Form 941,

Employer’s Quarterly

Federal Tax Return

, and Form 1040-X. For e-filed tax returns, the processing status reflects the

typical number of days it currently takes to process a form after receipt from the taxpayer. For

paper tax returns, the processing status reflects which month of receipt is currently being

processed. As of March 18, 2024, the IRS is currently processing paper Forms 1040 received in

March 2024.

11

TIGTA, Report No. 2024-400-006,

Final Results of the 2023 Filing Season

(Nov. 2023).

Page 11

Interim Results of the 2024 Filing Season

Finally, the IRS also allows taxpayers to create an online account, which is a safe and easy way

for individual taxpayers to view specific details about their Federal tax account. For example,

taxpayers can view the amount owed on their account, payment history, and key information

from their most current tax return filed,

etc

. There are 39.5 million IRS.gov online accounts that

have been created as of February 29, 2024.

Social media platforms

The IRS also offers taxpayers the ability to obtain information from the IRS using their mobile

devices. For example, the IRS uses common social media platforms to share the latest

information on tax changes, scam alerts, initiatives, and products and services. In addition, the

IRS provides short, informative online videos in English, Spanish, Chinese, and American Sign

Language. As of March 6, 2024, the IRS reported more than 1.3 million followers on the various

social media platforms and 31.2 million views of its social media videos.

12

Toll-free telephone level of assistance

As of March 2, 2024, taxpayers made 18.4 million total call attempts and 12.6 million net call

attempts to contact the IRS by calling the various customer service toll-free telephone assistance

lines.

13

The IRS also reports that 4.1 million calls were answered with automation, and telephone

assistors answered nearly 4.3 million calls and provided a 91 percent Level of Service with a

2-minute Average Speed of Answer. Figure 9 shows a comparison of toll-free performance for

Calendar Years 2023 and 2024, as of March 2, 2024. The Level of Access, which TIGTA

developed because the IRS’s Level of Service measure did not reflect overall call demand, was

51.2 percent.

Figure 9: Toll-Free Performance

Statistics for Calendar Years 2023 and 2024

Statistic

Filing Season

2023

2024

Assistor Calls Answered 3,840,311 4,329,437

IRS Calculated Level of Service 82.1% 91.0%

Average Speed of Answer (Minutes) 5 2

TIGTA-Developed Level of Access

14

54.0% 51.2%

Source: IRS management information reports (as of March 4, 2023, for

Calendar Year 2023 and as of March 2, 2024, for Calendar Year 2024).

12

Individuals may use more than one social media platform; therefore, it would not be appropriate to consider the

total number of followers as unique individuals.

13

Total call attempts represent calls received during all hours, open or not. This figure would include taxpayer

hang-ups prior to selecting service. Total net call attempts represent calls received during open hours after removing

transfers among product lines.

14

The Level of Access reflects the total of callers seeking assistance who receive it and is computed by taking the sum

of Assistor Calls Answered and Automated Calls Answered divided by the Total Dialed Number Attempts Open Hours.

TIGTA developed this metric in 2019 because the IRS’s Level of Service measure did not reflect overall call demand.

This is not an official IRS statistic.

Page 12

Interim Results of the 2024 Filing Season

In November 2023, TIGTA reported that the IRS met the Secretary of the Treasury’s expectations

for the 2023 Filing Season reporting a level of service average of 85.2 percent as well as

reducing the average wait time to answer a taxpayer’s call to approximately three minutes.

15

However, the report noted that improvements are needed to ensure that taxpayers receive top

quality service when contacting customer service telephone lines. TIGTA made four

recommendations, including that the IRS evaluate the availability of resources to provide quality

customer service on the telephone lines and ensure that all telephone lines that place callers on

hold provide information on tax scams as legislatively required. The IRS agreed with each of

TIGTA’s recommendations. In addition, TIGTA is conducting a review to assess the IRS’s efforts

to improve toll-free access and reduce taxpayer wait times when calling for assistance and plans

to issue a report later in Calendar Year 2024.

16

The TACs

The IRS plans to assist about 2 million taxpayers at its TACs in Fiscal Year 2024, which is an

increase of 22 percent from the number of taxpayers the IRS assisted during Fiscal Year 2023.

Figure 10 shows the number of contacts by product line at the TACs for Fiscal Years 2023 and

2024.

Figure 10: TAC Contacts for

Fiscal Years 2023 and 2024

Contacts/Product Lines

Fiscal Year

2023

Actual

2024

Projections

Tax Account Contacts 953,000

1,117,000

Form Contacts 52,000

61,000

Other Contacts 586,000

763,000

Tax Law Contacts 11,000

13,000

Totals

1,602,000

1,954,000

Source: IRS management information reports. Numbers

shown are rounded.

Insufficient staffing continues to result in the TACs not being open to provide taxpayer

assistance. As of March 4, 2024, the IRS reported that 17 of the 363 TACs were closed due to a

lack of staffing. IRS management cautioned that the operating status of the TACs can vary

day-to-day due to illness, staff leaving, or staff taking other positions within the IRS. For

example, as of March 9, 2024, 155 of the 363 TACs the IRS operated were staffed with one or

two IRS employees.

Similar to prior filing seasons, the IRS continues to use its appointment service for all TACs.

When taxpayers call to schedule an appointment, the IRS will attempt to resolve the taxpayer’s

question or provide the taxpayer with information on alternative services in order to prevent the

15

TIGTA, Report No. 2024-IE-R001,

Actions Are Needed to Improve the Quality of Customer Service in Telephone

Operations

(Nov. 2023).

16

TIGTA, Audit No. 202310017,

Taxpayer Access to Telephone Service.

Page 13

Interim Results of the 2024 Filing Season

need for an in-person visit. As of February 24, 2024, the IRS reported that IRS employees

answered 718,446 calls to schedule an appointment. Of these, 397,962 calls necessitated that

the taxpayer schedule an appointment and visit a TAC, and 320,484 taxpayers were assisted

without having to visit a TAC.

In an effort to further assist taxpayers, on February 14, 2024, the IRS announced special

Saturday hours at more than 50 locations for face-to-face help between February and May 2024.

The IRS is offering service at select TACs on each of four monthly Saturdays beginning

February 24, 2024, and ending May 18, 2024. On these dates, the centers provide taxpayers with

in-person help between 9:00 a.m. and 4:00 p.m., and no appointments are required. The IRS

website posts information regarding the days and hours of operation and a list of services

provided as well as whether the TAC is open on one of these four Saturday dates. According to

IRS management, they have served 7,661 taxpayers in the 89 TACs that were open on

February 24, 2024, and March 16, 2024.

Finally, in addition to the services offered via the TAC appointment line and at the TACs, the IRS

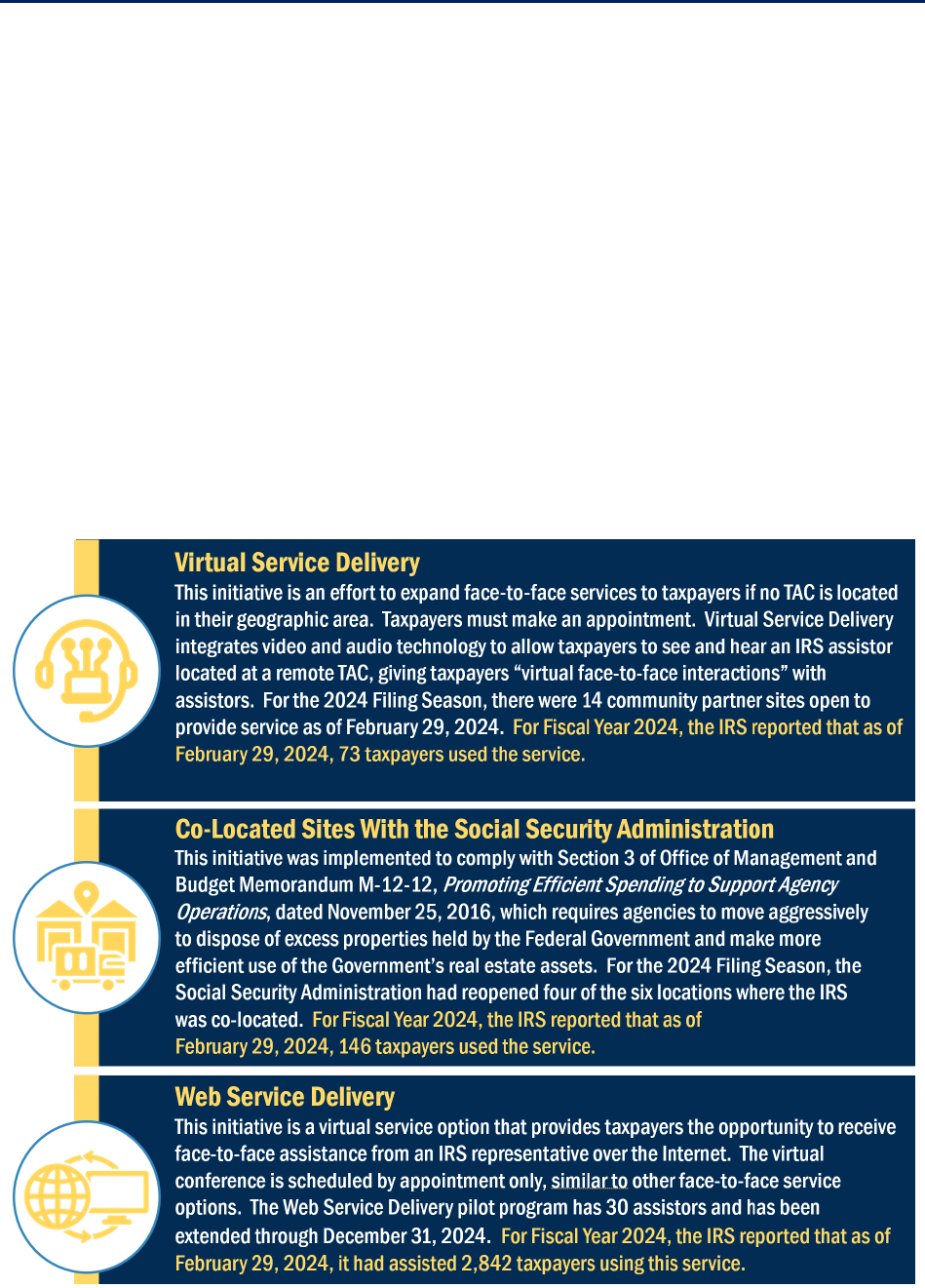

also offers these additional face-to-face initiatives, as summarized in Figure 11.

Figure 11: Summary of IRS Face-to-Face Initiatives

Source: IRS management information reports.

Page 14

Interim Results of the 2024 Filing Season

TIGTA is conducting a review of the quality of service provided to taxpayers at the TACs and

plans to issue a report later in Calendar Year 2024.

17

Assistance at Volunteer Program sites

The Volunteer Program plays an important role in the IRS’s efforts to improve taxpayer service

and facilitate participation in the tax system. The two main components in the Volunteer

Program are the Volunteer Income Tax Assistance and the Tax Counseling for the Elderly

programs. These programs provide no-cost tax return preparation and e-filing to underserved

taxpayer segments, including low-income, elderly, disabled, rural, limited-English-proficient, and

Native American taxpayers. As of March 4, 2024, Volunteer Program sites prepared more than

1 million tax returns at 8,261 Volunteer Program sites. Figure 12 shows the number of tax

returns prepared by volunteers for Fiscal Years 2023 and 2024, as of March 4, 2024.

Figure 12: Volunteer Program Statistics for Fiscal Years 2023 and 2024

(as of March 4, 2024)

Fiscal Year 2023 Fiscal Year 2024 Percentage Change

Tax Returns 1,005,092 1,048,048 4.3%

Sites 8,035 8,261 2.8%

Source: IRS management report showing the number of tax returns prepared for Fiscal

Years 2023 and 2024, as of March 5, 2023, and March 3, 2024, and the number of Volunteer

Income Tax Assistance sites as of March 6, 2023, and March 4, 2024. Percentages are rounded.

17

TIGTA, Audit No. 202210036,

Taxpayer Assistance Centers Generally Provided Quality Service, but Additional

Actions Are Needed to Reduce Taxpayer Burden.

Page 15

Interim Results of the 2024 Filing Season

Appendix I

Detailed Objective, Scope, and Methodology

The overall objective of this review was to evaluate whether the IRS timely and accurately

processed individual paper and e-filed tax returns during the 2024 Filing Season. To accomplish

our objective, we:

• Identified volumes of paper and e-filed tax returns received through March 2, 2024, from

the IRS Weekly Filing Season reports that provide filing season statistics and compared

the statistics to the same period for the 2023 Filing Season.

• Determined whether IRS monitoring systems indicate that individual tax returns were

being processed timely and accurately. We monitored key IRS indicators, including the

volume of tax return receipts, statistics from the IRS Filing Season Statistics Report, and

Error Resolution volumes.

• Ensured that select business rules associated with the implementation of key tax

provisions worked as intended. We evaluated the accuracy of the new business rules.

• Monitored current processing year volumes of inventory and monitored for any backlogs

of inventory from Calendar Year 2023 using IRS reports.

• Obtained information related to Submission Processing and Accounts Management

hiring and onboarding efforts.

• Identified results of the IRS tax refund fraud programs, including identity theft and

prisoner refund fraud.

• Identified results of the IRS customer service programs, including the TAC Program, the

Toll-Free Telephone Assistance Program, and the Volunteer Program.

• Identified results for the IRS’s self-assistance options, including IRS.gov and the social

media platforms.

Performance of This Review

This review was performed with information obtained from the Wage and Investment personnel

in Atlanta, Georgia, and the Wage and Investment Division Submission Processing personnel in

Covington, Kentucky, and the New Carrollton Federal Building in Lanham, Maryland, during the

period October 2023 through March 2024. We conducted this performance audit in accordance

with generally accepted government auditing standards. Those standards require that we plan

and perform the audit to obtain sufficient, appropriate evidence to provide a reasonable basis

for our findings and conclusions based on our audit objective. We believe that the evidence

obtained provides a reasonable basis for our findings and conclusions based on our audit

objective.

Major contributors to the report were Diana M. Tengesdal, Assistant Inspector General for Audit

(Returns Processing and Account Services); Sharla J. Robinson, Director; Tracy M. Hernandez,

Audit Manager; Jordan D. Bunte, Lead Auditor; Cally Sessions, Senior Auditor; Nathan J. Cabello,

Auditor; Branden L. Dreher, Auditor; Hong Cao, Information Technology Specialist;

Page 16

Interim Results of the 2024 Filing Season

Ismael Hernandez, Information Technology Specialist, and Theodore Logothetti, Information

Technology Specialist.

Data Validation Methodology

During this review, we obtained extracts from the Modernized Tax Return Database for

Processing Year 2024. Before relying on the data, we ensured that each file contained the

specific data elements we requested. In addition, we selected judgmental samples of each

extract and verified that the data in the extracts were the same as the data captured in the

Employee User Portal database. We also performed analysis on the Modernized Tax Return

Database extracts to ensure the validity and reasonableness of our data, such as ranges of dollar

values and obvious invalid values. We determined that the data were sufficiently reliable for

purposes of this report.

Internal Controls Methodology

Internal controls relate to management’s plans, methods, and procedures used to meet their

mission, goals, and objectives. Internal controls include the processes and procedures for

planning, organizing, directing, and controlling program operations. They include the systems

for measuring, reporting, and monitoring program performance. We determined that the

following internal controls were relevant to our audit objective: the process for planning,

organizing, directing, and controlling program operations for the 2024 Filing Season. We

evaluated these controls by monitoring IRS weekly production meetings, reviewing IRS

procedures, and reviewing IRS reports.

Page 17

Interim Results of the 2024 Filing Season

Appendix II

Treasury Inspector General for Tax Administration Audits

of Inflation Reduction Act of 2022 Tax Law Changes

This table presents in-process or planned TIGTA audits that will evaluate IRA provisions related

to the filing and processing of individual tax returns.

Audit Number Audit Title

2024408011 Inflation Reduction Act: Direct File Pilot Program

2024408016

Inflation Reduction Act: Registration for Elective Payment and Transfer

Elections Through the Energy Credits Online Portal

202340825

Inflation Reduction Act: Review of Implementation Efforts on the New Clean,

Commercial, and Previously Owned Vehicle Credits

Source: TIGTA Fiscal Year 2024 Annual Audit Plan.

Page 18

Interim Results of the 2024 Filing Season

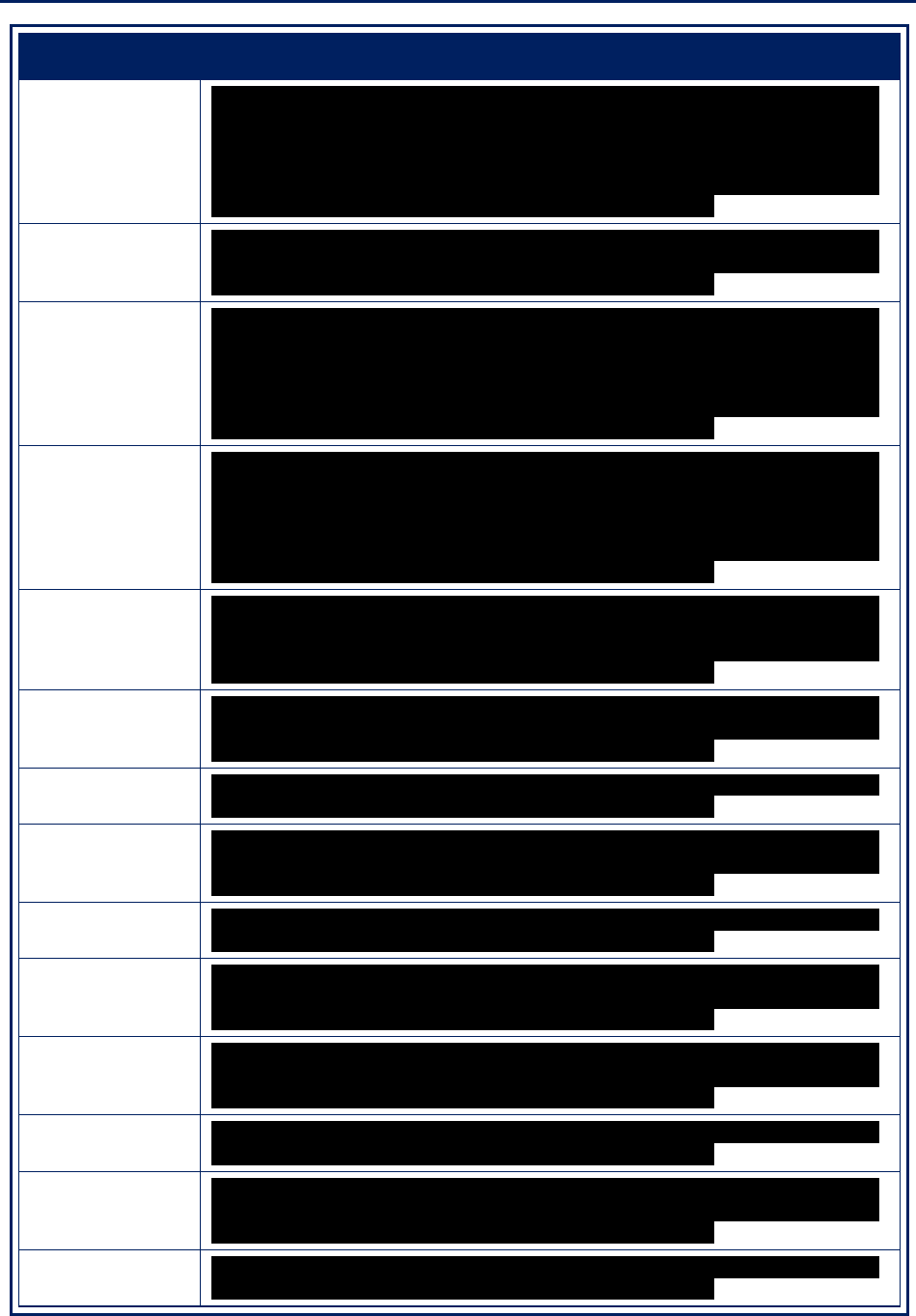

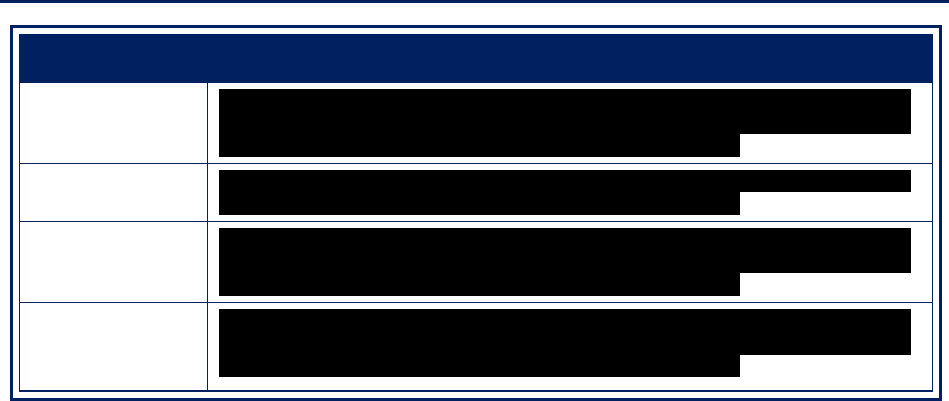

Appendix III

Electronic Filing Business Rules

Figure 1 presents a description of the 56 e-file business rules we reviewed that were created or

modified for the 2024 Filing Season.

Figure 1: Business Rules Reviewed for the 2024 Filing Season

Business Rule

Description

F1040-064-06 ****************************2******************************

****************************2******************************

****************************2******************************

****************************2******************************

****************************2******************************

****************************2***************.

F1040-471 ****************************2******************************

****************************2******************************

****************************2******************************

****************************2******************************

****************************2***************.

F5329-004 ****************************2******************************

****************************2******************************

****************************2***************.

F5329-005 ****************************2******************************

****************************2******************************

****************************2***************.

F5329-006 ****************************2******************************

****************************2******************************

****************************2***************.

F5695-007-04 ****************************2******************************

****************************2******************************

****************************2***************************.

F5695-030-01 ****************************2******************************

****************************2***************.

F5695-032 ****************************2******************************

****************************2******************************

****************************2***************.

F5695-033 ****************************2******************************

****************************2******************************

****************************2***************.

F5695-034 ****************************2******************************

****************************2******************************

****************************2******************************

****************************2******************************

****************************2***************.

F5695-035 ****************************2******************************

****************************2******************************

****************************2***************.

Page 19

Interim Results of the 2024 Filing Season

Business Rule

Description

F5695-036 ****************************2******************************

****************************2******************************

****************************2***************.

F5695-037

****************************2******************************

****************************2******************************

****************************2******************************

****************************2******************************

****************************2******************************

****************************2***************.

F5695-038 ****************************2******************************

****************************2***************.

F5695-039 ****************************2******************************

****************************2***************.

F5695-040 ****************************2******************************

****************************2***************.

F5695-041 ****************************2******************************

****************************2***************.

F5695-042 ****************************2******************************

****************************2******************************

****************************2***************.

F5695-043 ****************************2******************************

****************************2******************************

****************************2***************.

F5695-044 ****************************2******************************

****************************2******************************

****************************2******************************

****************************2******************************

****************************2******************************

****************************2******************************

****************************2******************************

****************************2***************.

F5695-045 ****************************2******************************

****************************2******************************

****************************2******************************

****************************2******************************

****************************2******************************

****************************2******************************

****************************2******************************

****************************2***************.

F5695-046 ****************************2******************************

****************************2***************.

F5695-047 ****************************2******************************

****************************2***************.

F5695-048 ****************************2******************************

****************************2***************.

F5695-049 ****************************2******************************

****************************2***************.

Page 20

Interim Results of the 2024 Filing Season

Business Rule

Description

F5695-050 ****************************2******************************

****************************2******************************

****************************2***************.

F5695-051 ****************************2******************************

****************************2***************.

F5695-052 ****************************2******************************

****************************2******************************

****************************2***************.

F5695-053

****************************2******************************

****************************2******************************

****************************2******************************

****************************2******************************

****************************2******************************

****************************2******************************

****************************2***************.

F5695-054 ****************************2******************************

****************************2******************************

****************************2***************.

F8283-036 ****************************2******************************

****************************2******************************

****************************2******************************

****************************2******************************

****************************2***************.

F8283-037 ****************************2******************************

****************************2***************.

F8283-039 ****************************2******************************

****************************2***************.

F8889-004 ****************************2******************************

****************************2******************************

****************************2***************.

F8889-005 ****************************2******************************

****************************2******************************

****************************2******************************

****************************2******************************

****************************2******************************

****************************2***************.

F8889-006 ****************************2******************************

****************************2***************.

F8889-007 ****************************2******************************

****************************2******************************

****************************2***************.

F8889-008 ****************************2******************************

****************************2******************************

****************************2***************.

Page 21

Interim Results of the 2024 Filing Season

Business Rule

Description

F8889-009 ****************************2******************************

****************************2******************************

****************************2******************************

****************************2******************************

****************************2******************************

****************************2***************.

F8889-010 ****************************2******************************

****************************2******************************

****************************2***************.

F8889-011 ****************************2******************************

****************************2******************************

****************************2******************************

****************************2******************************

****************************2******************************

****************************2***************.

F8889-012 ****************************2******************************

****************************2******************************

****************************2******************************

****************************2******************************

****************************2******************************

****************************2***************.

F8889-013 ****************************2******************************

****************************2******************************

****************************2******************************

****************************2***************.

F8889-014 ****************************2******************************

****************************2******************************

****************************2***************.

F8889-015 ****************************2******************************

****************************2***************.

S3-F1040-024 ****************************2******************************

****************************2******************************

****************************2***************.

S3-F1040-026 ****************************2******************************

****************************2***************.

S3-F1040-028 ****************************2******************************

****************************2******************************

****************************2***************.

S3-F1040-029 ****************************2******************************

****************************2******************************

****************************2***************.

S3-F1040-156 ****************************2******************************

****************************2***************.

SC-F1040-023 ****************************2******************************

****************************2******************************

****************************2***************.

SC-F1040-024 ****************************2******************************

****************************2***************.

Page 22

Interim Results of the 2024 Filing Season

Business Rule

Description

SF-F1040-015-01 ****************************2******************************

****************************2******************************

****************************2***************.

SF-F1040-024 ****************************2******************************

****************************2***************.

SH-F1040-025 ****************************2******************************

****************************2******************************

****************************2***************.

SSE-F1040-026 ****************************2******************************

****************************2******************************

****************************2***************.

Source: IRS business rule list.

Page 23

Interim Results of the 2024 Filing Season

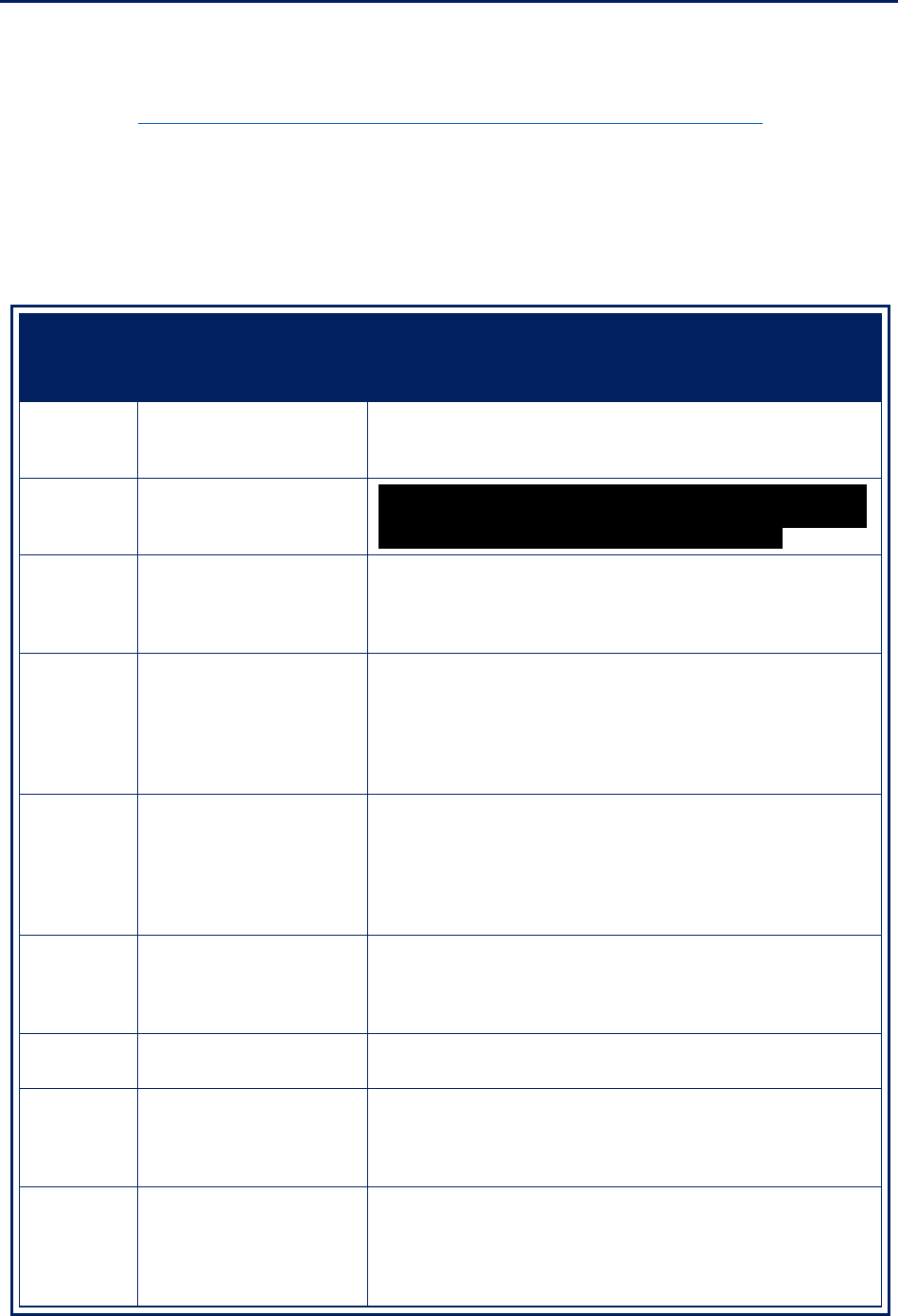

Appendix IV

Tax Return Errors Resolved Using the FixERS Tool

The IRS is using the FixERS tool during the 2024 Filing Season to address 23 common taxpayer

errors for individual tax return filers. Figure 1 provides a brief description of the Error Resolution

codes addressed using the FixERS tool.

Figure 1: FixERS Codes for the 2024 Filing Season

Error

Resolution

Code

Topic of

Error Resolution Code

Description

017 ITIN Status Code Sets when the ITIN Status Code is “I,” meaning it is inactive

for either the Primary, Secondary, any Dependent, or either

Child Care Credit Dependent.

029 Unclaimed Credits

*********************2**********************

*********************2**********************

*********************2**************.

034 Filing Status Code Sets when the Filing Status Code is inconsistent with the

requirements needed to claim the Filing Status. Filing Status

Codes 4, 5, and 7 require the taxpayer to also claim

dependents in order to qualify for that Standard Deduction.

075 Taxable Social Security

Verified Amount

Sets when the Taxable Social Security Verified amount is not

present. The only entries on the return are Total or Taxable

Social Security and Withholding, with the Refund equaling the

Withholding. Additionally, it will catch returns where the

taxpayer does not list Taxable Social Security; however, there

is an indication of a Lump Sum Election.

121 Excess Social

Security Withholding and

Railroad Retirement Tax

Act

Sets when the taxpayer’s figure for Excess Social Security or

Railroad Retirement Tax Act Withholding is equal to or greater

than the computer’s computation. In order to claim this

withholding, the taxpayer must have more than one employer

and the combined withholding must exceed the limitation

amounts.

214 Taxable Social

Security Benefits

Sets when the taxpayer did not correctly figure their Taxable

Social Security Benefits amount. This calculation is based on

amounts claimed in other fields of the return, including their

Gross Taxable Social Security amount.

248 Qualified Business

Income Deduction

Sets when the Qualified Business Income Deduction amount

is not supported by business income reported on the return.

280 CDCC Sets when the taxpayer’s amount for the CDCC and the

computer’s calculation for this credit differ. This can be

caused by a miscalculation by the taxpayer or by an action

taken in a previous error code.

287 Child and Other

Dependent Credit and the

Additional Child Tax

Credit (ACTC)

Sets when the difference between Child and Other Dependent

Credit and the computer’s calculation is greater than $2. It

will also generate when the difference between the

ACTC/Refundable Child Tax Credit and the computer’s

calculation is greater than $2.

Page 24

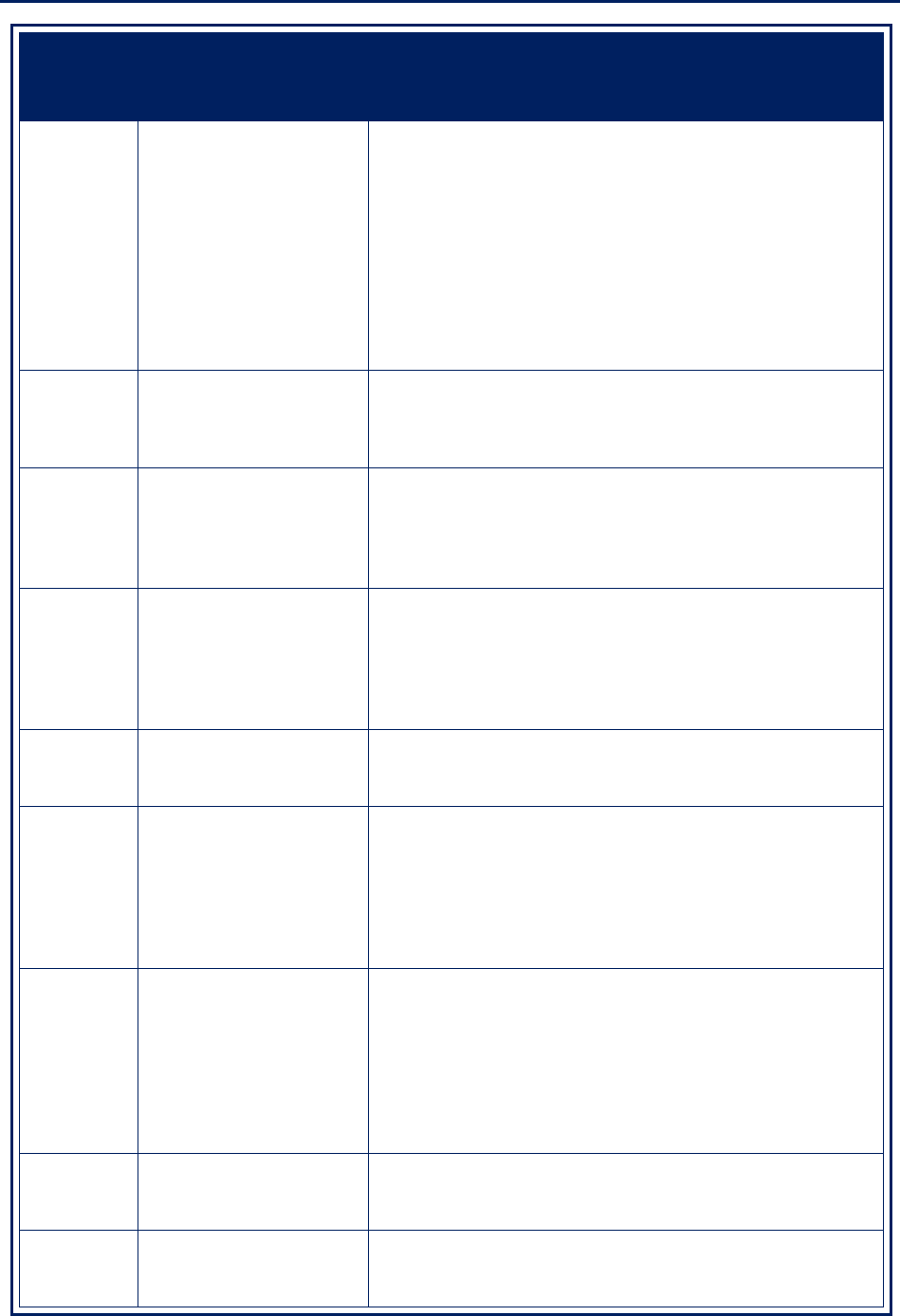

Interim Results of the 2024 Filing Season

Error

Resolution

Code

Topic of

Error Resolution Code

Description

289 Total Children Eligible for

the CTC

Sets when the Total Children Eligible for the CTC and/or total

number of dependents eligible for Credit for Other

Dependents are present, and any of Forms 8839, Qualified

Adoption Expenses, 8396, Mortgage Interest Credit, 8859,

Carryforward of the District of Columbia First-Time

Homebuyer Credit, 8834, Qualified Electric Vehicle Credit,

8912, Credit to Holders of Tax Credit Bonds, 8978, Partner’s

Additional Reporting Tax Year, or Other Credits are present,

and either the CTC and Other Dependent Credit Verified is not

present or the ACTC Verified and Refundable CTC Verified is

not present.

290 Child and Other

Dependent Credit

Sets when a math error is present between the taxpayer’s

amount for Child and Other Dependent Credit and the

computer’s amount, and the taxpayer’s amount and the

computer amount for Total Tax do not agree.

291 Residential Clean Energy

Credit and Energy

Efficient Home

Improvement Credit

Sets when a math error is present between the taxpayer’s

amount for Residential Clean Energy Credit or Energy Efficient

Home Improvement Credit and the computer’s amount, and

the taxpayer’s Total Tax Liability and the computer’s amount

for Total Tax do not agree.

298 Clean Vehicle Credit and

Previously Owned Vehicle

Credit

Sets when the Tax Period is 202312 and later and one or

more invalid conditions exist, such as the taxpayer’s Clean

Vehicle Credit or Previously Owned Vehicle Credit amounts do

not agree with the computer’s amount, non-matching entries

on Form 8936, Clean Vehicle Credits, and Schedule A (Form

8936), or the presence of Special Processing Code ‘R’.

328 First-Time Homebuyer

Credit

Sets when it appears the Primary and/or Secondary taxpayer

must repay their First-Time Homebuyer Credit and are not

making any payments on their return.

329 Repayment of First-Time

Homebuyer Credit

Sets when the Primary and/or Secondary taxpayer are

repaying their First-Time Homebuyer Credit; however, a math

error is present. This may occur if the Secondary taxpayer

listed their Taxpayer Identification Number on the repayment

form; however, the credit is under the Primary taxpayer’s SSN,

etc. This may also occur if they are paying over or under the

amount they owe each year.

336 Earned Income Credit

(EIC)

Sets when the taxpayer is claiming the EIC and an error is

present with either the Primary, Secondary, or a Dependent’s

Taxpayer Identification Number Assignment Date, i.e., the

Taxpayer Identification Number Assignment Date is later than

the due date of the return. This may also generate if

Schedule EIC is present and EIC Amount is significant and the

number of EIC SSNs present does not equal the computer’s

amount in Qualified EIC Dependent Number.

337 EIC With Schedule EIC Sets when the amount claimed for the EIC differs from the

computer amount and Schedule EIC is present, meaning

dependents are claimed for the credit.

338 EIC Without Schedule EIC Sets when the amount for EIC differs from the computer

amount and Schedule EIC is not present, dependents are not

being claimed for the credit.

Page 25

Interim Results of the 2024 Filing Season

Error

Resolution

Code

Topic of

Error Resolution Code

Description

344 ACTC not Tax Year 2021 Sets when the Tax Period is not Tax Year 2021, the taxpayer

amount for the ACTC differs from the computer’s amount, and

Total Payments is not equal to Total Payments Computer.

345 ACTC Tax Year 2021 This affects Tax Year 2021 only. Generates when the

taxpayer’s amount for the ACTC differs from the computer’s

amount, and Total Payments is not equal to Total Payments

Computer.

350 RRC Tax Year 2021 This affects Tax Year 2021 only. Generates when the

taxpayer’s amount for the RRC differs from the computer’s

amount, and Total Payments does not equal Total Payments

computer. The taxpayer did not correctly report their RRC

amount.

363 CDCC Tax Year 2021 This affects Tax Year 2021 only. Sets when the taxpayer’s

amount for the CDCC and the computer’s calculation for this

credit differ. This can be caused by a miscalculation by the

taxpayer or by an action taken in a previous error code. For

example, if a dependent is disqualified in error code 017

because their ITIN is inactive, and this dependent is claimed

for the CDCC, it will change the calculation causing a math

error to set. This may also be caused by taxpayer failure to

check the Principal Abode Box on Form 2441, allowing the

refundable portion of this credit.

601 Total Tax Exceeds

50 Percent of Adjusted

Gross Income

Generates when the taxpayer’s Total Tax reported exceeds

50 percent of their adjusted gross income. Tax examiners are

instructed to check for transcription errors and verify the tax

claimed.

Source: IRS management-provided list of error codes and descriptions.

Page 26

Interim Results of the 2024 Filing Season

Appendix V

Glossary of Terms

Term Definition

Adjusted Gross Income

Gross income minus adjustments to income. Gross income includes wages,

dividends, capital gains, business income, and retirement distributions as

well as other income. Adjustments to income include such items as

educator expenses, student loan interest, alimony payments, or

contributions to a retirement account.

Business Rule

Used to validate information included on e-filed tax returns for acceptance

into tax return processing. The IRS will reject e-filed tax returns from

processing when the tax return does not meet a business rule.

Child and Dependent

Care Credit

A tax credit for expenses that are paid for the care of a qualifying individual

to enable taxpayers to work or to actively look for work.

Child Tax Credit A tax credit for families with qualifying children.

Earned Income Tax Credit A refundable tax credit for low-income to moderate-income workers.

Employee User Portal

The internal IRS portal that allows employees to access IRS data and

systems, such as tax administration processing systems and financial

information systems, in a secure, authenticated session.

Error Resolution

An online computer application used by tax examiners to correct errors

identified on individual or business tax returns during processing.

Error Resolution Code

These codes validate the accuracy of tax returns during processing. When

a return is identified with an error condition, the IRS suspends the return

from processing and sends it to a tax examiner to correct the error. Once

the error is corrected, the IRS continues to process the tax return.

Filing Season

The period from January 1 through mid-April when most individual income

tax returns are filed.

Fiscal Year

Any yearly accounting period, regardless of its relationship to a calendar

year. The Federal Government’s fiscal year begins on October 1 and ends

on September 30.

Free File

A free Federal tax preparation and e-filing program for eligible taxpayers

developed through a partnership between the IRS and the Free File, Inc.

(FFI). Free File, Inc. is a group of private sector tax software companies.

Integrated Data

Retrieval System

IRS computer system capable of retrieving or updating stored information.

It works in conjunction with a taxpayer’s account records.

Level of Access

The total number of calls seeking assistance that ultimately receive

assistance from the IRS. This is computed by taking the sum of Assistor

Calls Answered and Automated Calls Answered divided by Total Dialed

Number Attempts Open Hours.

Page 27

Interim Results of the 2024 Filing Season

Term Definition

Level of Service

The primary measure of service to taxpayers. It calculates the level of

service taxpayers who call the Accounts Management function’s toll-free

telephone lines have at speaking with an assistor. Further, it is a budget

measure used to determine the resources for the toll-free telephone lines.

The IRS’s measure is titled Customer Service Representative Level of

Service.

Master File

The IRS database that stores various types of taxpayer account information.

This database includes individual, business, and employee plans and

exempt organizations data.

Modernized Tax Return

Database

The official repository of all electronic returns processed through the

Modernized e-File system.

Paper Tax Returns Waiting

to Be Processed

Tax returns that have not yet been entered into the IRS’s tax processing

system.

Prisoner File

The IRS compiles a list of prisoners received from the Federal Bureau of

Prisons and State Departments of Corrections as well as Prisoner Update

Processing System data from the Social Security Administration.

Processing Year The calendar year in which the IRS processes the tax return or document.

Rejects

Tax returns that cannot be processed, usually due to missing or incomplete

information. Tax examiners correspond with the taxpayer to clarify an entry

on a return. When the taxpayer responds, the tax examiner will resolve the

issue and the return will continue processing.

Tax Examiner

An employee located in a field office who conducts examinations through

correspondence. However, the tax examiner position is also used for many